Inside Digital & eCommerce 2026 in 10 Charts – Brand Manufacturers

- Teresa Sperti

- Jun 3

- 7 min read

We have now delivered our 6th annual study in partnership with Six Degrees Executive titled Inside Digital & eCommerce 2026.

For this edition, we made a deliberate choice to move away from a broad industry view and go deeper on two closely connected sectors: retailers and brand manufacturers.

The findings land at a genuinely turbulent moment. A rare convergence of pressures is reshaping the landscape — consumer confidence has dropped to levels not seen since the COVID lockdowns, well below the decade average, and the drag on discretionary spending is real. Geopolitical headwinds are still working their way through the economy. And AI and agentic commerce are fundamentally changing how people shop — shaping up to be the defining disruption of the decade.

The overarching theme emerging from the findings is that complexity is accelerating faster than capability. Brands understand where growth will come from and are investing heavily in product content, digital shelf, AI, retail media, loyalty and omnichannel experiences. Yet capability, resource constraints, and fragmented execution continue to make it difficult to realise the full value of those investments.

The brands pulling ahead are not necessarily the ones doing more. They are the ones who have clarity over where to play and how to win and are building the discrete capabilities required to compete in a far more fragmented ecosystem.

We’ve rounded up the top 10 charts that provide an insight into the state of the market for brand manufacturers (CPGs, FMCGs and industrial brands) based on our study findings.

So many channels to manage, so little time and resource: eCommerce channel adoption for brand manufacturers

The days of managing a retailer website and a DTC site are long gone.

Nearly half of all brand manufacturers are now managing five or more commerce channels, while more than one in five are managing ten or more. Marketplaces, social commerce, quick commerce, retailer websites, owned channels and emerging conversational commerce environments have created an increasingly fragmented landscape.

The challenge isn't simply being present across more channels. It's maintaining consistent product content, brand experience and pricing, ensuring strong availability, and maximising visibility across all of them.

More channels create more opportunity, but it also creates more places to fail.

The brands winning today are becoming increasingly selective about where they play, while investing in automation, digital shelf analytics and AI to manage growing complexity.

Managing the product presence | PDP is painful for many

Product content has rapidly moved from an operational task to a strategic capability.

Improving product content and digital shelf execution was cited as the number one eCommerce priority by brand manufacturers this year. Yet despite the focus, only 26.3% of leaders believe retailers and marketplaces provide a seamless process for sharing and optimising product content.

This creates a challenging dynamic. Brands are investing heavily in content, imagery, product attributes and AI readiness, while many retailers do not have mechanisms to enable content to be published and optimised in real time which creates brand risk and hampers retail media effectiveness.

In an era where product content influences search visibility, AI recommendations, conversion and compliance, delays and inefficiencies are no longer just operational headaches. They directly impact revenue and share.

Influencing the path to purchase in a rising sea of private label brands has never been so important

As retailer private label ranges continue to expand and improve, brands are recognising they can no longer rely solely on retailers to drive preference.

More than 82% of brand manufacturers now view delivering seamless omnichannel experiences as a strategic priority, while almost half are prioritising loyalty initiatives.

The common thread is clear. Brands are looking for more ways to influence the shopper's journey beyond the shelf.

Whether through loyalty programs, DTC experiences, content ecosystems or retail media, the objective is the same: build stronger connections with shoppers before a purchasing decision is made.

The brands that create direct relationships and build first-party data assets will have significantly more influence over future growth than those relying exclusively on retailers to build that shopper relationship.

A mix of more traditional and modern loyalty approaches are on the roadmap for brands over the next 12 – 18 months

For years, loyalty was largely viewed as the retailer's domain. That is changing.

Nearly one third of brands are planning to introduce or expand brand-owned loyalty programs, while more than one in five are exploring subscription-based models. Competitions, retailer loyalty participation and rewards programs also feature prominently in future plans.

This reflects a broader shift occurring across the market. Brands are increasingly recognising that driving sales beyond a campaign to deliver sustained growth requires a different approach. One that supports one to one relationship through data, strong value exchanges beyond the product itself and an ability to engage ongoing with thos loyalty is not simply about repeat purchase behaviour. It is about data, relationships and creating value exchanges that strengthen long-term customer connections.

As customer acquisition becomes more expensive and retail competition intensifies, loyalty is emerging as an increasingly important strategic asset.

More brands than retailers believe AI and agentic commerce will have a significant impact on how shoppers buy

An overwhelming 96% of brand leaders believe AI and agentic commerce will have a moderate or significant impact on how shoppers buy, with 71% expecting the impact to be significant.

That level of conviction reflects how exposed brands are to shifts in discoverability.

Historically, brands optimised for retailer search algorithms and physical shelf placement. Increasingly they must optimise for AI recommendations, conversational commerce environments and agentic shopping assistants.

The path to purchase is being rewritten in real time.

50% of leaders say they are adapting their search and discoverability strategy for AI, which means 50% aren’t. 34% are yet to adapt at all.

One of the most striking findings in the study is the split between brands responding to AI-driven discovery and those still watching from the sidelines.

Half of brand manufacturers are adapting their search and discoverability strategies for AI environments. They are investing in GEO, structured product content, AI visibility and discoverability.

At the same time, 34% have yet to adapt or act at all. This is a significant risk.

Brands that fail to optimise product data and content for AI environments risk becoming invisible during the discovery phase, regardless of how strong their products are.

The winners in AI commerce may not simply be the brands with the best products. They may be the brands that are easiest for AI systems to understand, interpret and recommend.

Brands spoilt for choice with retail media networks

The Australian retail media market continues to expand rapidly.

Almost half of all brands are now leveraging four or more retail media networks, and many categories now have an extensive range of network options spanning grocery, pharmacy, beauty, department store, marketplace and specialty retail environments.

This creates opportunity, but also complexity.

Brands are increasingly being asked to manage multiple networks, multiple measurement frameworks, multiple formats and multiple retailer relationships.

The challenge is shifting from whether to invest in retail media to determining where investment can generate the greatest return.

Amazon ads no longer a sleeping giant

The growth of Amazon Ads should serve as a warning sign for every retail media network operating locally.

Brand adoption has jumped from 33% in 2025 to 52.8% in 2026, making Amazon one of the most widely utilised retail media platforms in Australia.

This is hardly surprising.

Amazon has had two decades to refine its advertising offering, measurement capabilities and targeting infrastructure. It combines retail media, marketplace data and sophisticated attribution in ways many local networks are still working towards.

The challenge for Australian retail media networks is not simply competing with each other. It is closing the capability gap with Amazon before advertiser budgets increasingly follow performance.

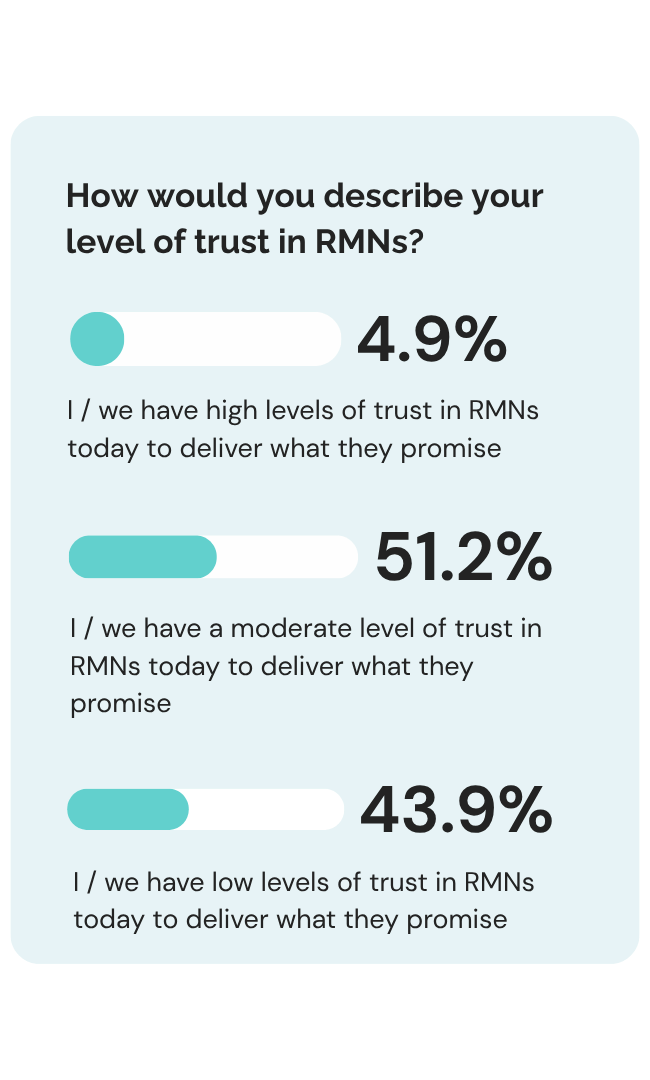

Trust in retail media networks remains low – even though investment intentions are high

Despite growing investment intentions, trust remains stubbornly low.

Just 4.9% of brand leaders report high levels of trust in retail media networks to deliver on their promises, while 43.9% express low levels of trust.

This is perhaps the most important finding in the entire retail media section.

The issue isn't demand. Brands want to invest. The issue is confidence.

Measurement inconsistencies, limited attribution, fragmented reporting and varying levels of network maturity continue to undermine trust.

Retail media has firmly established itself as a major revenue stream for retailers. The next phase of growth will depend on whether networks can prove value consistently and transparently.

AI & eCommerce tools are topping the list of MarTech investment priorities as brands focus on digital shelf and AI

AI tools are now the number one MarTech investment priority for brand manufacturers.

At the same time, investment in digital asset management, digital shelf analytics, eCommerce platforms and customer data capabilities continues to accelerate.

Yet there is a contradiction emerging.

Not a single leader expressed high confidence that their current data and technology foundations are ready to support AI-driven use cases, and more than half report low confidence.

The enthusiasm for AI is real but the foundations required to fully leverage it are still catching up.

The brands that succeed over the next three years will likely be those that spend less time chasing the latest AI capability and more time strengthening the product, customer and technology foundations that allow AI to create meaningful value.

The overarching theme from this year's study is clear: ambition is high, but capability gaps remain significant.

Brand manufacturers understand where growth will come from. They understand the importance of AI, product content, retail media, loyalty and omnichannel experiences.

The challenge now is execution. In a market becoming more fragmented, more competitive and more AI-driven by the day, the brands that build the strongest foundations today will be the ones best positioned to win tomorrow.

About the report

The Inside Digital & eCommerce 2026 Report is produced by Arktic Fox and Six Degrees Executive and draws on insights from more than 100 Australian marketing, digital, eCommerce and retail media leaders across retail and brand manufacturer organisations.

The study was conducted between February and April 2026 through two tailored 41-question surveys designed specifically for retailers and brand manufacturers.

The report explores the evolving priorities, capabilities and challenges shaping AI, omnichannel, loyalty, retail media, eCommerce, marTech and digital shelf strategy across the Australian market.